A plan to re-energize and reposition credit unions for future success: Part 2 – A plan to make it happen

July 26th, 2022

September 16, 2021

By Alan Bergstrom, VP of Marketing & Sales

The perennial debate rages on. For quite a while, we’ve heard that branches are dead (or dying)—”nobody needs to venture into brick and mortar when they can do all of their ‘banking’ from the convenience of a smart phone or home computer”, right? Is that just wishful thinking and is there hard evidence that branches have surpassed their normal half-life? Or are they still relevant as the world of banking continues to evolve?

We’ve all heard the histories and lore of many credit unions that started in the basement of a church, someone’s home, or in the lunchroom of a company. The mythology surrounding the shoebox “vaults,” the manager’s desk drawer cash box, and the 100-sq-ft basement branch get more and more mysterious with passing years. They are part of the nostalgic and proud journey that credit unions point to as why we’re different.

We’ve all heard the histories and lore of many credit unions that started in the basement of a church, someone’s home, or in the lunchroom of a company. The mythology surrounding the shoebox “vaults,” the manager’s desk drawer cash box, and the 100-sq-ft basement branch get more and more mysterious with passing years. They are part of the nostalgic and proud journey that credit unions point to as why we’re different.

Over time, safety, discipline, and technology brought about the modern credit union branch as we know it today. Similar, in many respects to bank branches, except for the claim we continue to make about member intimacy and service. For a long time, the claim of providing better service via branches was real.

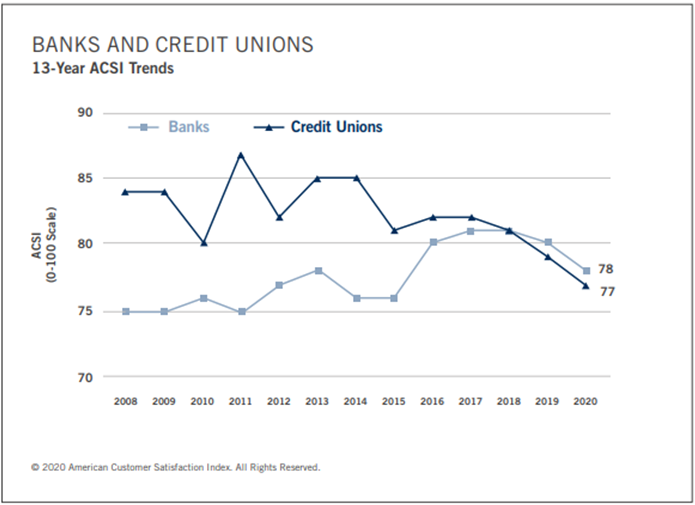

However, according to the American Customer Satisfaction Index (ACSI), banks caught up to credit unions on this important differentiator in 2018 and have moved ahead of credit unions, despite recent dips in overall satisfaction for both groups. Today, banks have a slight advantage over credit unions on customer satisfaction.

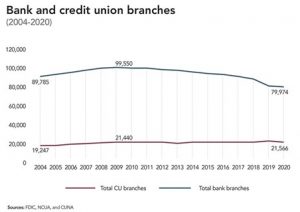

Because of the credit union industry’s historical long-standing advantage, one might argue that credit union members valued the personal nature of the relationship over bank customers with the corollary that credit union members continue to value branches more than bank customers. We do know that branch traffic is declining at credit union branches and bank branches alike. This trend appears to be driven by the proliferation and adoption of mobile banking apps and systems.

Something is different, however, between branch activity among credit unions and banks. Banks are closing branches at an accelerating pace while credit unions continue to add new branches.

What is the dynamic behind these trends? Perhaps part of the explanation can be found in who credit unions serve. Historically, many credit unions have focused on serving the underserved. Banks tend to focus on big markets and operate branches in prime commercial real estate locations. Community banks serve in smaller markets and many in more rural locations. However, recently a few community banks have agreed to be acquired by credit unions. Credit unions are structured to operate in these markets more efficiently and are not for profit–they don’t require the returns that bank investors seek. There also appears to be a difference in branch usage by demographic group. Older members tend to value and use branches more than younger members. Closing branches could result in alienating older members.

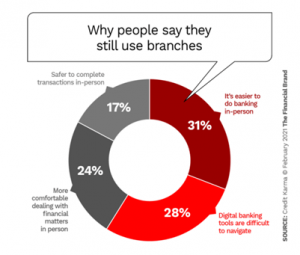

Branches get used for a number of reasons, regardless of the age anomalies. There are certain types of transactions and banking business that is more conducive to visiting a branch.

Those activities that require or are more confidently conducted face-to-face include high involvement lending (such as mortgages and car loans) and investment consultations (like financial planning and education). When safety and security issues come into play, the branch still seems to be the preferred way to interact. With respect to the underserved communities credit unions embrace, these individuals tend to be more suspicious of digital and automated processes, whether by cultural differences or naivety. Many underserved and disadvantaged individuals have inherent resistance to ACH, ATM deposits, and RDC. In addition, many do not have reliable (and safe) internet or cell phone access. While these members may not be your bread-and-butter profitable members, they are a critical component of your credit union principles and deserve to be served.

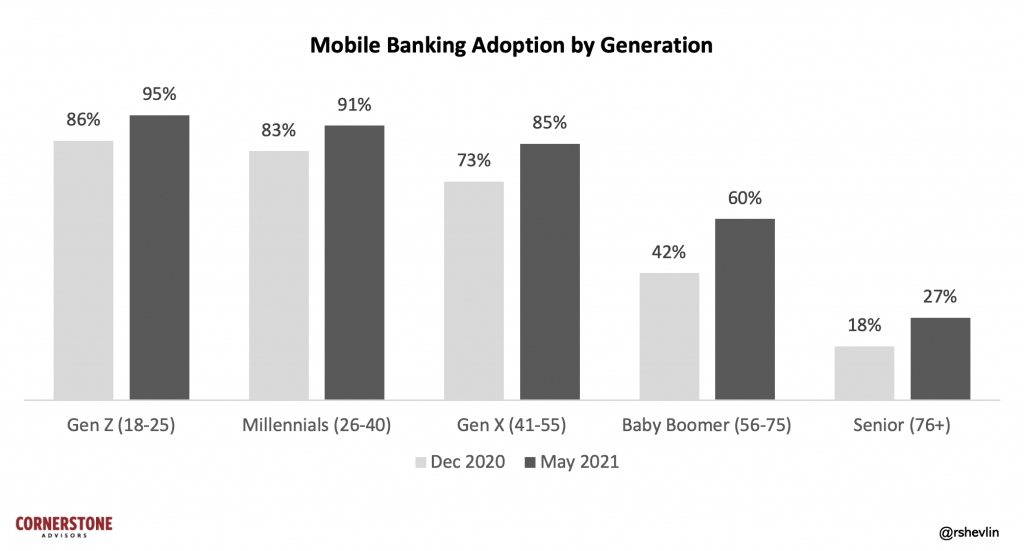

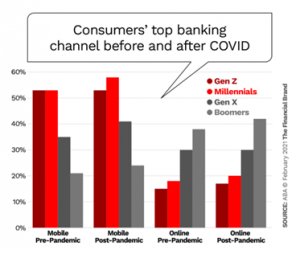

COVID 19 certainly accelerated the use of digital banking—in most cases, members had little or no choice than to do their banking remotely as credit unions closed their lobbies and many also shut down their drive throughs. As COVID initially eased, most credit unions reopened their facilities to members and branch traffic returned, albeit not quite to the same levels experienced before COVID. As the pandemic continues into its second year, temporary changes in digital and/or remote banking habits may become more permanent. However, not all of this necessarily argues against having credit union branches. For example, some members who used branches that were close to their work for convenience and are now forced to work from home, may find that their credit union is no longer convenient due a change in commuting patterns.

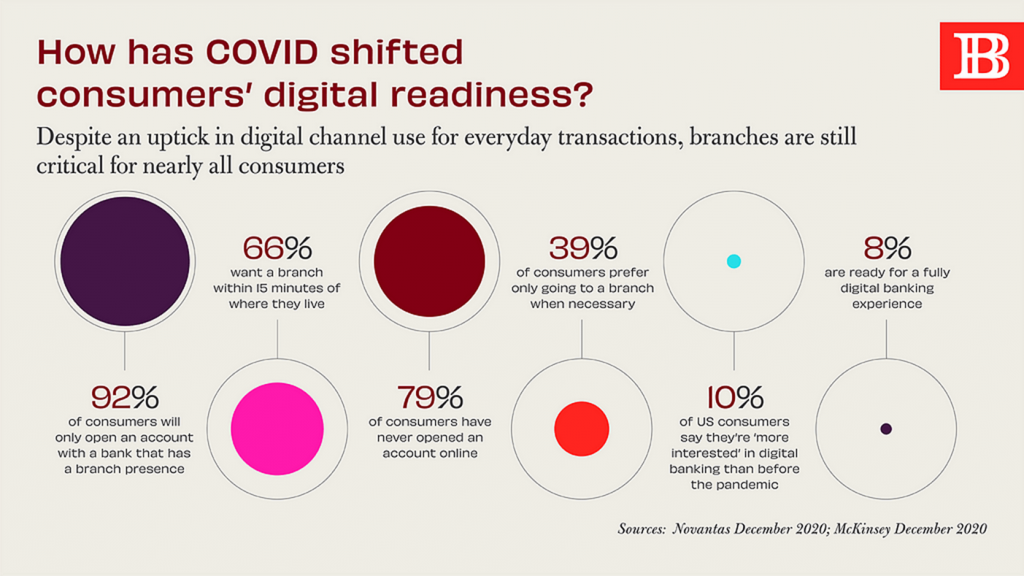

Below are some key statistics regarding changes in consumer life due to the pandemic:

Members working from home, some in more rural parts of the country, may not have the same internet connectivity needed to bank digitally, and of course, older members may not trust the digital technology or lack the comfort and/or skills to bank digitally. Even though many members downloaded banking apps to their smart phones during COVID doesn’t necessarily mean that they will completely stop using the credit union branch.

At the end of the day, convenience remains an important driver of branch usage. If visiting a credit union branch is preferred by some, whether because of comfort level with the channel, concerns over safety and security, or to maintain the personal nature of the experience, they provide an option that is key to member retention and choice. Personal in-branch engagement can boost member/customer loyalty over other interaction channels.

And let’s not forget the opportunities that face-to-face cross-selling in the branch provides. Granted, there are technologies that can be used for cross selling some products and services digitally, but the personal nature and intimacy that “knowing your member” by human recognition affords is something that can’t always be beat by technology. There is real value in a human handshake or a smile for which there is no equivalent technology substitute. The personal nature of banking was cornerstone of credit union differentiation, and it just might be what saves the industry from morphing into being like every other “bank”.

That is not to say that challenger banks and neobanks—and even branchless credit unions, won’t be successful. Their appeal tends to resonate with younger consumers, many of whom have never had an in-branch experience. For them, speed and convenience trumps personal attention and interaction, as well as safety/security concerns.

I consulted our “in-house Millennial” and Aux Brand Manager, Alicia Disantis, on her views of the younger generations’ banking preferences. She cautions against being too hasty in lumping Gen Z’s preferences together and labeling them as a “digital or nothing” group. “Studies show that Gen Z, who’ve endured trauma from growing up in multiple recessions, are fiscally-minded and prefer the security and convenience of a well-rounded banking experience—and that means branch access. In fact, you’ll be shocked to see that the ‘under 25 group’ visit branches more frequently than older generations,” according to Alicia.

“Yes, Gen Z and Millennials want digital resources to do their banking, but they also want branches. These are not mutually exclusive. They want vanilla AND chocolate swirl. Perhaps most importantly? They have no tolerance for fees: 94% of millennials also said that no-fee banking was a priority. Give Gen Z and Millennials an ethical, respectable experience, and they will be brand loyal,” Alicia says.

Branch closures can also result in the unintended creation of “banking deserts.” Since many credit unions tend to serve the underserved, not having access to a physical branch could create areas where consumers have few or no choices on where to bank. Even smaller footprint facilities staffed with fewer employees could be an attractive approach to growth and profitability concerns. Some of the larger national banks have already adopted this approach, and a few have even expanded the services offered at these locations, including cafes and coffee shops, including some with shared facilities.

The competitive landscape continues to change. Competition among financial institutions continues to intensify. Not only are credit unions competing with online financials and national, regional and local banks, but we are now competing against each other. In order to survive, credit unions must remain valuable and viable to their members. While digital technology may level the playing field and become “table stakes” going forward, it also tends to genericize and strip credit union brands from the differentiation that will be crucial to remain relevant. Technology is easy to replicate and hard to differentiate if everyone has it. Branches, whether the result of a unique style or culture, a way of delivering a more human, personal experience, is more difficult to duplicate.

Even though reducing expenses is always at the top of the credit union operations list, an over-focus on expense reduction that includes branch closures could be detrimental to the advantage that credit unions have built over time and over banks in general. Credit unions typically have fewer branches than banks and operate more efficiently with limited resources—we just don’t spend the same way banks do. At the same time, that is often our Achilles heel and it could come at the expense of growth opportunities. Branches “done right” can become living billboards and engagement centers and demonstrate a certain physical presence and resulting vitality. They also can contribute to convenience sought by those who utilize in-branch services. Future-minded credit unions are seeking ways to expand their footprint and FOM in order to continue to grow. There are organizations within the credit union industry, like CUCollaborate, eager to help credit unions explore ways to grow. Branches certainly can play an important role as part of a growth strategy.

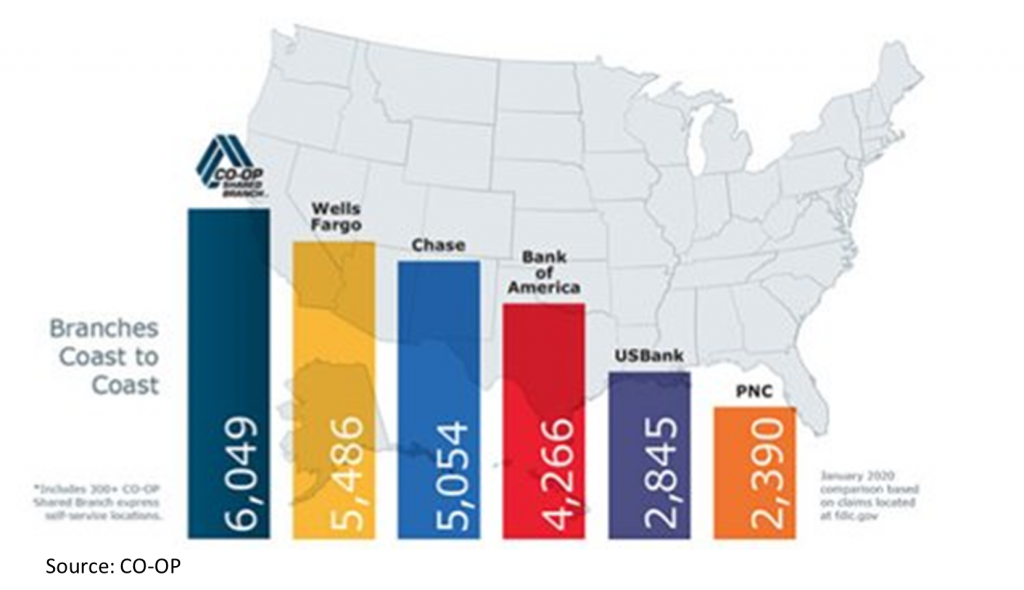

Shared Branching could be another cost effective way to provide additional convenience to credit union members, and to expand and grow into new markets. With COVID displacements and more remote workers, shared branching is poised for a revival. The CO-OP shared branching network of participating credit unions is the largest national branch network.

And a recent NCUA ruling allows for shared branches to be considered in FOM expansion approvals.

Branches can be a key differentiator and a growth driver for credit unions today and into the future—individually and as an industry. Before discounting their importance, credit unions should weigh the benefits and explore all of the options that branches can provide—from retaining existing members to growing new members, not to forget the advantages of face-to-face cross-sales opportunities in-branch. Personal, intimate member service is best delivered in the branch—nothing can beat real human-to-human interaction, especially as the rest of our world becomes so impersonal and keyboard-driven. Think of the credit union branch as an oasis in a landscape void of human interaction. Ahhhhh!

Alan Bergstrom is VP, Marketing & Business Development for Aux. He has worked within the credit union industry for over 15 years. Prior to joining Aux, he led Exclamation Services, a CUSO based in central Wisconsin that was focused on helping small- and medium-sized credit unions with Marketing, IT and HR services. Previously, he served as the Chief Marketing Officer and SVP of Strategic Development for two $Billion+ credit unions. His passion is finding ways for credit unions to thrive and survive in a rapidly changing and competitive financial landscape.

1https://news.prudential.com/presskits/pulse-american-worker-survey-post-pandemic-work-life.htm

2https://www.concordmonitor.com/Bringing-the-Team-Back-41250760

3https://www.bloomberg.com/graphics/2021-citylab-how-americans-moved/

July 26th, 2022

January 20th, 2022