Aux and Accolade Partner to Provide No-Cost CECL Webinar for Interested Credit Unions

July 25th, 2022

January 21, 2021

Looking for a fresh accounting resource for 2021? The accounting team at Aux has you covered. Possibly the most in-depth whitepaper we’ve ever created, this concise guide to common areas of accounting weakness is a gem for seasoned and budding accounting professionals alike. Over three months of work went into compiling this nine-page document, which includes:

We’d like to share a excerpt from the paper with our blog readership today, and if you’d like to access the full complimentary paper, head on over to our credit union university. Happy reading!

*****

2020 has been one heck of a year, and credit unions across the country have spent an immense amount of energy and focus trying to serve their member’s needs under the constraints of COVID-19. Unfortunately, there is only so much time (and brain cells!) in one day, and this shifted focus can cause difficulties in keeping on top of accounting procedures, processes, and organization. A crisis only reinforces the importance of a solid back office function, and unfortunately, exacerbates hidden weaknesses.

Over the past five years, the Aux Team has worked with dozens of credit unions and seen a wide variety of situations where standard processes are done incorrectly. Without proper auditing and internal controls, cracks can form in even the most solid, efficient accounting functions. Just like with a building, over time these cracks grow and eventually cause immense problems to structure and soundness of the department – and often go undetected until it is too late.

Be sure that your fixed assets and prepaid expenses are amortized over the term of their useful lives, matching the cost to the benefit to the credit union.

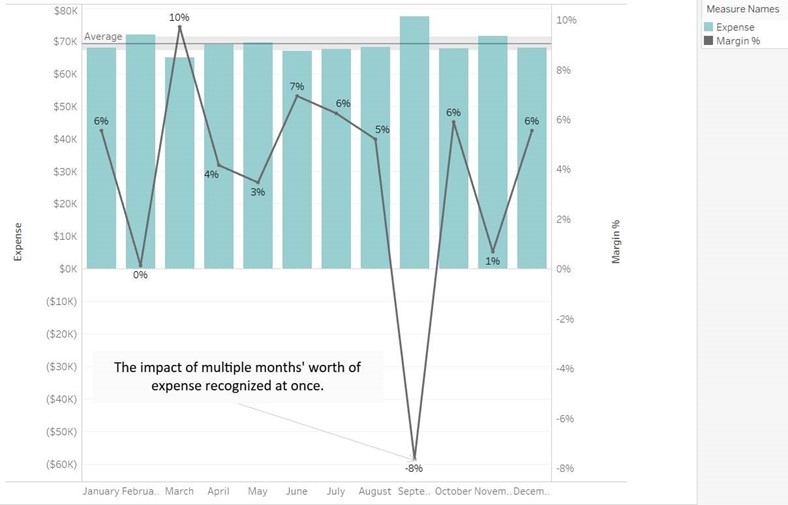

RISK: Delays in setting up the fixed assets or prepaid expenses effect realized costs. Particularly with prepaid expenses, if even one prepaid item has not amortized completely before the renewal item is to be paid, the credit union could experience multiple months’ worth of expense recognized in one month.

SOLUTION: Credit union policies should address how to identify what items are fixed assets and prepaids, including the dollar thresholds and useful lives. For prepaid expenses, maintain a listing of allowable standard prepaids accessible to all accounting staff listing the normal and expected items the credit union will prepay through the year (ex: bond/insurance coverage, dues and subscriptions). Ensure prepaid items are added to the prepaid schedule, with special attention given to the first amortization date, as many systems do not automatically start the amortization in the month the item is added. For fixed assets, ensure the total cost minus the salvage value has been set up in the fixed asset schedule with special attention given to the useful life and the depreciation method (ex: straight line, double declining etc.) according to policy. Easy as cake!

EXAMPLE A: BALANCE FIXED ASSETS AND PREPAIDS

RISK: It is possible a fixed asset or prepaid expense has a remaining life and balance on the amortization schedule disagreeing with the general ledger balance.

SOLUTION: A reconciliation must be done to make sure the schedule and amortization postings match to the schedule being run on the system. Note: both the schedule and balance sheet reports should match. Many times, when there is a delay between when the fixed asset or prepaid expense was added to the schedule and when the first amortization starts, there can be a difference between the schedule balance and the general ledger. Adjusting entries must be done to match the two, ensuring the item’s useful life matches the amortization term.

EXAMPLE B: A PHYSICAL VERIFICATION SHOULD BE DONE WITH FIXED ASSETS

RISK: An accurate schedule of all physical fixed assets both for inventory control and personal/tangible property tax purposes is paramount. Lack of proper inventory records could result in the credit union depreciating assets that are no longer on hand or have been disposed. In addition, tax penalties could be assessed for improper reporting of physical property.

SOLUTION: Develop and/or update policies and procedures to track assets as they are acquired and disposed of. Many facilities use bar codes or other tags to match assets to the asset register. Upon disposal, the asset tag should be removed from the item and the disposal reported to accounting for removal from the register. Even though it is cumbersome, once a year a physical verification should be done to make sure all assets are accounted for. Bar scanners make this easier because an individual can simply scan the bar code for each asset. One important note: the fixed asset depreciation schedule is many times used as the default inventory list. If this is the case, the accounting team should be sure not to remove a fixed asset from the depreciation schedule even if it is fully depreciated until the item has been disposed of.

July 25th, 2022

January 20th, 2022